NYC Teachers Retirement: A Comprehensive Guide to Securing Your Future

By Sophia Edwards

Retirement planning is one of the most critical aspects of financial stability for educators in New York City. NYC teachers retirement programs offer a robust framework designed to ensure that teachers can enjoy a secure and comfortable life after their dedicated service to education. Understanding these programs is essential for both current and aspiring educators who want to plan effectively for their post-career lives.

The education sector in New York City is one of the largest employers, and its retirement system plays a vital role in attracting and retaining top talent. By understanding the intricacies of NYC teachers retirement plans, educators can make informed decisions about their financial futures. This article will delve into every aspect of NYC teachers retirement programs, providing actionable insights and guidance.

Whether you're a new teacher just starting your career or a seasoned educator nearing retirement age, this guide will help you navigate the complex world of retirement planning. From understanding the benefits to optimizing your contributions, we'll cover everything you need to know to secure your financial well-being.

Understanding NYC Teachers Retirement System

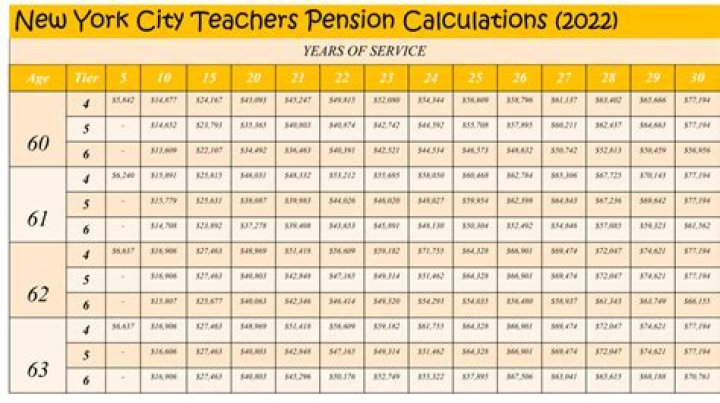

The NYC Teachers Retirement System (NYCTRS) is a defined benefit pension plan designed specifically for public school teachers in New York City. It provides eligible educators with a predictable income stream during retirement, ensuring financial security after decades of service. Understanding how this system works is crucial for making the most of its benefits.

Key features of the NYCTRS include:

- Defined Benefit Plan: Provides a guaranteed monthly income based on years of service and final average salary.

- Vesting Period: Teachers must work for a minimum of 10 years to become vested and eligible for retirement benefits.

- Contribution Rates: Teachers contribute a percentage of their salary to the retirement fund, which is matched by the city.

By participating in the NYCTRS, teachers can rest assured that their future financial needs will be met, allowing them to focus on their teaching responsibilities without worrying about post-retirement uncertainties.

Eligibility Criteria for NYC Teachers Retirement

To qualify for NYC Teachers Retirement benefits, educators must meet specific eligibility criteria. These criteria ensure that only those who have demonstrated long-term commitment to the education system can access the benefits of the retirement plan.

Years of Service Requirement

One of the primary eligibility factors is the number of years an educator has served in the NYC public school system. Generally, teachers must accumulate at least 10 years of credited service to become vested. However, the exact requirements may vary based on individual circumstances and tier membership.

Age Requirements

Retirement age is another critical factor. Most teachers can retire at age 55 with at least 25 years of service or at age 62 with at least 10 years of service. Early retirement options are also available, though they may result in reduced benefits.

Tier Membership

The NYCTRS operates under different tiers, each with its own set of rules and benefits. The tier a teacher belongs to depends on when they joined the system:

- Tier 1: Members who joined before April 1, 1996

- Tier 2: Members who joined between April 1, 1996, and December 31, 2009

- Tier 3: Members who joined on or after January 1, 2010

Understanding your tier is essential for determining your retirement benefits and contribution rates.

NYC Teachers Retirement Benefits

The NYCTRS offers a range of benefits designed to support educators during their retirement years. These benefits go beyond the basic pension and include additional financial protections and healthcare options.

Pension Benefits

Pension benefits are calculated based on factors such as years of service, final average salary, and retirement age. The formula varies depending on the tier, but generally, the pension is calculated as a percentage of the final average salary multiplied by the number of years of service.

Healthcare Coverage

Eligible retirees can continue to receive healthcare coverage through the NYC Municipal Retiree Health Benefits Program. This program provides comprehensive medical, dental, and vision coverage, helping retirees maintain their well-being without incurring significant out-of-pocket expenses.

Death and Disability Benefits

In the event of death or disability, the NYCTRS offers benefits to protect the financial security of the teacher's dependents. These benefits may include survivor pensions, disability payments, and life insurance coverage.

How to Maximize NYC Teachers Retirement Benefits

Maximizing your retirement benefits requires careful planning and strategic decision-making. Here are some tips to help you get the most out of your NYC Teachers Retirement plan:

Understand Your Contribution Rates

Teachers contribute a percentage of their salary to the retirement fund. Understanding your contribution rate and how it impacts your future benefits is crucial. Higher contributions can lead to increased pension benefits upon retirement.

Plan for Early Retirement

If early retirement is a consideration, it's important to understand how it will affect your benefits. While early retirement is possible, it may result in reduced pension payments. Planning accordingly can help mitigate these effects.

Supplement with Additional Savings

In addition to the NYCTRS, teachers should consider supplementing their retirement savings through other vehicles, such as 403(b) plans or individual retirement accounts (IRAs). These additional savings can provide extra financial security during retirement.

NYC Teachers Retirement Plan vs. Other Retirement Plans

While the NYCTRS is specifically tailored for NYC teachers, it's worth comparing it to other retirement plans to understand its unique advantages and limitations.

Defined Benefit vs. Defined Contribution Plans

The NYCTRS is a defined benefit plan, which guarantees a specific monthly income during retirement. In contrast, defined contribution plans, like 401(k) or 403(b) plans, depend on investment performance and contributions, making them less predictable but potentially more lucrative.

Public vs. Private Sector Retirement Plans

Public sector retirement plans, like the NYCTRS, often offer more comprehensive benefits than private sector plans. They typically include guaranteed pensions, healthcare coverage, and other protections that may not be available in private sector plans.

Tax Implications

Understanding the tax implications of retirement benefits is essential. Pension payments from the NYCTRS are generally taxable, but healthcare benefits may be tax-free. Consulting with a tax professional can help teachers optimize their retirement income.

Steps to Enroll in NYC Teachers Retirement

Enrolling in the NYCTRS is a straightforward process, but it requires attention to detail to ensure all necessary steps are completed correctly.

Complete the Enrollment Form

New teachers must complete the enrollment form provided by the NYC Department of Education. This form collects essential information about the teacher's employment status and contribution preferences.

Submit Required Documentation

Along with the enrollment form, teachers must submit any required documentation, such as proof of employment or identification. Ensuring all documents are accurate and up-to-date is crucial for a smooth enrollment process.

Stay Informed About Updates

Regularly checking for updates from the NYCTRS is important, as changes in legislation or policy can affect retirement benefits. Staying informed ensures teachers can adapt their plans accordingly.

Common Misconceptions About NYC Teachers Retirement

There are several misconceptions surrounding NYC Teachers Retirement that can lead to confusion or misinformation. Addressing these misconceptions is essential for making informed decisions.

Myth: Teachers Automatically Enroll in the NYCTRS

While most teachers are automatically enrolled in the NYCTRS, it's important to verify enrollment and ensure all necessary paperwork is completed. Teachers should confirm their enrollment status with their employer or the retirement system.

Myth: Pension Benefits Are Guaranteed Forever

While pension benefits are generally secure, they are subject to changes in legislation or funding. Teachers should stay informed about potential changes that could affect their benefits.

Myth: Contributions Are Optional

Contributions to the NYCTRS are mandatory for all eligible teachers. Failure to contribute can result in reduced benefits or loss of eligibility. Understanding the contribution requirements is essential for maintaining retirement benefits.

Financial Planning for NYC Teachers Retirement

Effective financial planning is critical for ensuring a comfortable retirement. Teachers should consider several key factors when planning for their post-career lives.

Estimate Retirement Expenses

Calculating estimated retirement expenses helps teachers determine how much they need to save. Factors such as housing, healthcare, and leisure activities should be considered when estimating these expenses.

Create a Retirement Budget

A detailed retirement budget can help teachers allocate their resources effectively. By planning for both essential and discretionary expenses, teachers can ensure their retirement funds last throughout their post-career years.

Consult a Financial Advisor

Seeking advice from a qualified financial advisor can provide valuable insights into retirement planning. Advisors can help teachers optimize their savings, investments, and retirement benefits to achieve their financial goals.

Resources for NYC Teachers Retirement

Several resources are available to help teachers navigate the NYC Teachers Retirement system. These resources provide valuable information and support to ensure teachers make informed decisions about their retirement.

NYCTRS Official Website

The official NYCTRS website offers comprehensive information about retirement benefits, enrollment processes, and updates. Teachers can access detailed guides, forms, and contact information for further assistance.

NYC Department of Education

The NYC Department of Education provides resources and support for teachers regarding retirement planning. Teachers can consult with HR representatives or access online resources to learn more about their retirement options.

Retirement Planning Seminars

Many organizations offer retirement planning seminars specifically for NYC teachers. These seminars provide valuable insights into maximizing retirement benefits and addressing common concerns.

Conclusion

Navigating the NYC Teachers Retirement system requires a thorough understanding of its features, benefits, and requirements. By staying informed and planning effectively, teachers can secure a stable and comfortable retirement. This comprehensive guide has covered everything from eligibility criteria to financial planning strategies, ensuring educators are well-prepared for their post-career lives.

We encourage all NYC teachers to take advantage of the resources available and consult with financial advisors to optimize their retirement plans. Share this article with colleagues and explore other resources on our website to further enhance your knowledge of retirement planning.

![Decoding Movie Rules: Understanding & Enjoying Films | [Movierulz] & Beyond](https://silver.isevcloud.co.uk/uploads/3-movierulz-brings-the-latest-hollywood-movierulz-news-3movierulz-also-brings-movie-news-tv-news-trailers-reviews-movierulz-articles-in-south-ind-movies-are-more-than-just-a-form-of-entertainment-they-are-a-reflection-of-culture-storytelling-and-human-emotions-understanding-the-rules-that-govern-films-can-enhance-your-viewing-experience-and-provide-deeper-insights-into-the-narratives-presented-in-this-article-we-will-explore-the-five-essential-movie-rules-that-every-cinephile-should-know-before-movierulz-2025-latest-hd-telugu-kannada-tamil-south-indian-movies-web-series-shows-kdramas-watch-at-high-quality-on-movierulz-tv-this-page-is-intended-to-document-significant-changes-to-the-movie-rules-over-the-course-of-the-site-u2019s-history-this-is-far-from-a-complete-list-with-emphasis-being-placed-on-more-recent-rule-changes-standard-goals-based-on-di-u2026-understanding-movierules-is-essential-for-filmmakers-producers-and-even-audiences-these-regulations-impact-everything-from-the-production-phase-to-distribution-and-viewership-by-adhering-to-these-rules-filmmakers-can-navigate-the-complex-landscape-of-content-creation-ensuring-their-work-is-both-legally-compliant-and-culturally-sensitive-movie-show-times-schedules-and-tickets-in-los-angeles-long-beach-anaheim-santa-ana-irvine-burbank-lakewood-santa-monica-fountain-valley-orange-pasadena-ca-when-it-comes-to-enjoying-films-understanding-the-core-principles-that-govern-cinematic-storytelling-can-elevate-your-viewing-experience-significantly-the-5-movie-rules-com-framework-offers-a-set-of-guidelines-designed-to-help-both-filmmakers-and-audiences-appreciate-the-intricacies-of-modern-cinema-in-this-article-we-will-explore-these-five-essential-rules-and-this-combination-of-comfort-variety-and-free-access-makes-movierulz-profoundly-attractive-especially-for-viewers-on-a-tight-budget-the-dark-side-of-piracy-we-would-like-to-show-you-a-description-here-but-the-site-won-u2019t-allow-us-movierulz-com-movierulz-latest-bollywood-and-hollywood-movies-watch-online-full-free-movierulz-is-wide-range-collection-of-telugu-movies-tamil-malayalam-bengali-kannada-movierulz-movierulz-provide-a-wide-range-of-telugu-movies-tamil-malayalam-and-hindi-movies-watch-full-telugu-movies-online-anytime-anywhere-on-zee5-also-explore-41-telugu-movies-online-in-full-hd-from-our-latest-telugu-movies-collection-movies-are-more-than-just-a-form-of-entertainment-they-are-a-reflection-of-culture-storytelling-and-human-emotions-understanding-the-rules-that-govern-films-can-enhance-your-viewing-experience-and-provide-deeper-insights-into-the-narratives-presented-in-this-article-we-will-explore-the-five-essential-movie-rules-that-every-cinephile-should-know-before-movierulz-latest-featured-telugu-movies-watch-online-download-full-free-collection-of-bollywood-movies-tamil-malayalam-dubbed-kannada-5movierulz-movierulz-is-a-piracy-website-that-leaks-the-tamil-telugu-kannada-hindi-movies-and-allows-users-to-download-movies-in-free-check-out-the-latest-news-and-updates-on-meta-movierulz-here-enjoy-watching-new-telugu-movies-release-of-2025-experience-the-latest-and-new-south-indian-movies-on-your-mobile-device_720.jpg)